Contact Us

Contact Us

Individuals and Families

Individuals and Families

Institutional Expertise. Individual Service.

We can help with every aspect of your personal and business finances—from working around concentrated positions to creating income for life, from building businesses to liquidating them, and from focused to growing wealth to focused designing legacies that pass on wealth and values to future generations—and beyond.

FINANCIAL PLANNING:

At Premier Wealth Partners, we start the financial planning process with a detailed understanding of your long-term goals. We want to understand what motivates our clients and articulate their long-term needs. Next, we create a tailored Financial Plan which will illustrate where you are today and how to get to where you want to be in the future. This process will allow us to identify any issues/obstacles that may prevent you from realizing your dreams. Once the Financial Plan is complete, specific recommendations will be made based on your risk tolerance and priorities. Lastly, we will collaborate with you to update your financial plan as your needs and goals change over time.

INVESTMENT MANAGEMENT:

Once a customized Financial Plan is delivered to our client, we will then agree upon action steps to implement results-focused investment strategies. Our job will then be to implement and monitor your portfolio strategically and tactically through rebalancing and investment selection. Our approach is designed to pursue competitive risk-adjusted returns that match each client’s financial goals, values, and risk tolerance.

Our investment management services include:

- Customized advice based upon the client’s risk profile.

- Portfolio construction

- Asset allocation

- Portfolio risk management

- Ongoing monitoring with strategic and tactical rebalancing

- Performance reporting

Our team is committed to assisting you with your financial needs with the goal of providing specific investment and wealth planning strategies customized to you and your objectives.

Tactical allocation may involve more frequent buying and selling of assets and will tend to generate higher transaction cost. Investors should consider the tax consequences of moving positions more frequently.

Rebalancing a portfolio may cause investors to incur tax liabilities.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification, rebalancing and/or asset allocation does not protect against market risk.

RISK MANAGEMENT:

We all know that unfortunate life events occur, but some people feel that these occurrences will not happen to them or that they will have time to address it when a situation arises. The reality is that when something happens, it is too late to plan for.

Every risk we face can be addressed in one of the following ways:

- Risk Avoidance

- Risk Reduction

- Risk Transfer

- Risk Retention

The primary question that needs to be asked is what are the financial and emotional consequences to you and your family if various risks are not appropriately addressed?

Here at Premier Wealth Partners, we have risk management and insurance expertise to help you determine which solutions may suit you and your family’s needs. As part of our holistic planning process, we will help you determine if your current solutions are still adequate compared to when you originally purchased these risk management solutions.

For example, we can do a comparison analysis across various life and annuity carriers to determine which policies may offer the most value, strongest carrier credit rating, optimal product and rider features based upon your current (and not original) needs.

Return to Top

RETIREMENT PLANNING:

Much of today’s planning focuses on only getting to retirement. After crossing the finish line, many clients ask, “what’s next?”

Our experience has shown that crossing the finish line of retirement is where many individuals trip and fail to adequately regain the same trajectory.

Developing a plan that is consistent with your goals will improve your chances of finishing on the podium.

There are many variables to consider when planning for retirement. What can possibly go wrong when approaching retirement?

- How will I generate income to replace my salary?

- What investments should be sold and when?

- What are the tax implications for selling investments?

- How does my investment risk change after selling certain investments?

- Should my risk profile remain the same in pre-retirement and post retirement?

- How will my portfolio be impacted by sequence of returns risk?

- When should I claim Social Security benefits?

- What will my healthcare costs look like in retirement?

- What will happen to my affairs if I become sick or pass on?

- What is the best way to help my loved ones when I pass on?

- How should I gift to charities to provide the most impact now and down the road?

The list goes on and on.

It has been said that a plan without action is just a dream while a dream becomes a goal when action is taken towards achieving it.

Let’s work together to develop and execute a strategy tailored to your game plan.

Return to Top

INCOME STRATEGIES:

Many clients focus on the wealth accumulation phase during their working careers, but few people plan on the distribution phase during their retirement.

We firmly believe that an optimized investment management plan should be intertwined with developing appropriate income strategies.

While crossing the finish line into retirement is especially important, the next challenge is to continue the management of assets while making thoughtful decisions around where, what, and when to sell investments.

We are selective in the type of accounts (tax-deferred or after-tax accounts) we suggest, and strategic in the type of investments used in these accounts.

Our team will help to create a retirement income plan with the goal of providing a sustainable, predictable, and tax-efficient stream of income based upon your age, risk comfort level, personal values, and vision of retirement.

Return to Top

TAX PLANNING:

Many people pay more taxes than they need to. You and/or your beneficiaries may be able to pay less tax be implementing an asset location strategy within your portfolio, setting up a different type of retirement plan, reviewing your beneficiary designations, refinancing your mortgage, setting up a charitable fund, or carefully disposing a highly appreciated investment.

We will work with your Certified Public Accountant (CPA) or Enrolled Agent (EA) in an effort to minimize your taxes and ensure your tax preparation is as organized, effective, and simple as possible.

Return to Top

INCAPACITY PLANNING:

Establishing a “what if” plan or catastrophe plan before the unimaginable happens is priceless. Having seen firsthand when spouses, families, and other loved ones are thrust into positions in which they were completely unprepared, it is our mission at Premier Wealth Partners to plan for these events alongside you.

The financial industry has become focused on rate of return at the sacrifice of conversations like these.

If something happened to you tomorrow, who and how would the following questions be answered?

- Who would be responsible for these decisions?

- How would they feel handling the decisions?

- How much time could they dedicate to these topics each week or month?

- Where do these decision makers live and how close are they to you?

- Does this trusted person(s) have their own responsibilities including their families and their careers?

- What mistakes could be made?

- What would the true cost of mistakes?

- What action steps can we make now that will help them if that day comes sooner than planned?

At Premier Wealth Partners, we look to go beyond the typical “financial advisor-client” relationship, getting to know everyone important to you. Having planning meetings with clients, their beneficiaries, their Power of Attorney’s, and anyone the client feels deserves a seat at the table.

Return to Top

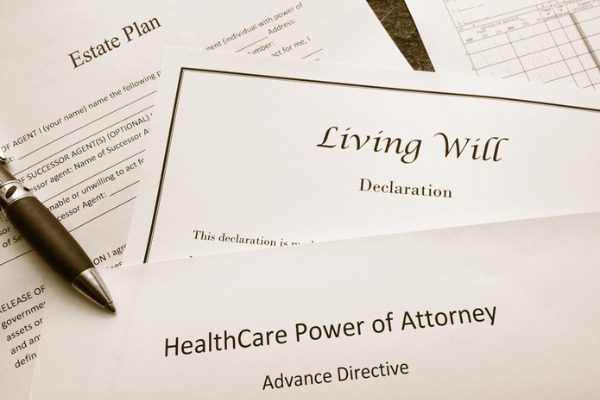

ESTATE PLANNING:

In many cases, clients assume that legal documents are “one and done” or “set it and forget it”, but this could not be any further from reality. Legal documents should be treated as “breathing documents” and they will need to be updated and amended as life events occur and/or as laws change.

Estate planning should be structured to help you create a comprehensive plan by working closely with your investment, tax, and legal advisors. Our goal is to work with these experts to help ensure all the moving parts of your plan are working together with the goal of benefiting you and your loved ones.

Effective estate planning strategies should be started when you are alive and in good health. The Premier Wealth Partners team will work with your trusted advisors to ensure the appropriate tools (life insurance, annuities, charitable trusts, beneficiary designations, etc.) are being used to address your current needs while managing your assets to be distributed according to your wishes.

You can control what happens tomorrow by planning today. We welcome the opportunity to help you enhance your legacy.

Return to Top

CHARITABLE GIVING:

Charitable giving means different things to different people. Aside from the potential estate and tax benefits, gifting provides personal enjoyment and satisfaction.

Charitable giving can be accomplished in many ways. Premier Wealth Partners will help you identify the advantageous ways to make an outright gift via a direct contribution or the donation of a particular asset. It is important to review your options.

Some examples of addressing your charitable goals include the following:

- Gifts from Individual Retirement Accounts

- Charitable Trusts

- Foundations

- Donor-Advised Funds

This material contains only general descriptions and is not a solicitation to sell any insurance product or security, nor is it intended as any financial or tax advice.

Riders are additional guarantee options that are available to an annuity or life insurance contract holder. While some riders are part of an existing contract, many others may carry additional fees, charges and restrictions, and the policy holder should review their contract carefully before purchasing. Guarantees are based on the claims paying ability of the issuing insurance company.